Freeman Law recently reported on the Cum-Ex tax scandal in The Biggest Tax Heist Ever? The Cum-Ex Scandal–an alleged fraud that has been dubbed by some as “the most complicated” tax fraud case in history. Since that time, the Eurpoean Union’s 55 billion euro cum-ex tax scandal has continued to expand. (See Two More Bankers Arrested in Germany Over Cum-Ex Scandal; A Private Bank That Survived the Nazis May Be Broken by German Tax Scandal. Two former London-based bankers were recently convicted in the first German trial to address the legality of the trading scheme that is at the center of the scandal. European governments and prosecutors claim that the scheme was a widespread criminal scandal involving hundreds of bankers, traders, lawyers, and others that rivals, if not exceeds, the likes of Enron. The trader/defendants maintain that they merely exploited a legal loophole.

The Cum-Ex Files is a joint investigation into an alleged tax fraud scheme that allegedly first began in 2001. In addition to the cum-ex scheme, governments have also focused on a lesser-known, and so-called cum-cum scheme. This post describes the basic mechanics of the cum-ex trading scheme.

The Cum-Ex Scheme

The cum-ex scheme was built on a so-called “cum-ex” trade—a practice that was outlawed in 2012. The cum-ex trade centers on an aggressive form of “dividend arbitrage” that gained notoriety in recent years in European countries.

A “cum-ex” trade was based upon a network of participants who would lend shares in a manner that created the appearance that there were two owners of the shares at the same time. This resulted in the issuance of a confirmation that tax on dividend payments had been paid, when in fact it had not. Multiple parties would then seek a “refund” of the dividend withheld tax.

As background, institutional investors may be entitled to claim a refund of dividend taxes from various European governments. In Germany, for example, until a 2012 change in the tax law, a dividend tax of 25% of the gross dividend was collected by the corporation that issued shares. The certificate for tax reimbursement, however, was issued by the shareholder’s bank. Depository institutions often issued reimbursement certificates incorrectly, which allowed multiple investors to claim refunds of such taxes, even though only one party had actually paid the dividend tax. (Again, using Germany as an example, the 2012 change in German tax law now provides that the depository institution is responsible for collecting the dividend tax and issuing reimbursement certificates.)

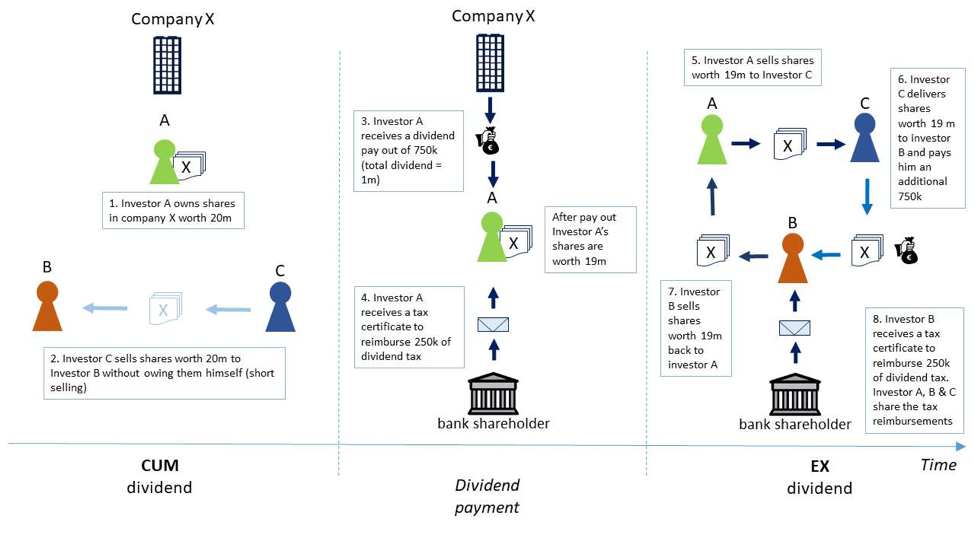

A Step-by-Step Outline of the Cum-Ex Scheme:

Here is a simplified example of how the alleged scheme works:

- Investor A (e.g. an asset manager) owns shares worth 20m in listed company X.

- Investor B now buys shares worth 20m from company X as well, just a few days prior to company X paying out dividend to its shareholders. The shares bought by investor B are characterized as cum-dividend shares, because these shares will provide the buyer with dividend. Investor B buys these shares from investor C, who does not own these shares himself yet. Investor C is ‘short-selling,’ and promises investor B to deliver the shares at an agreed time.

- Now company X pays out the dividend—worth 1m—to investor A, who receives €750.000 (directly from company X and a certificate from his own bank to reimburse €250.000) worth of dividend tax which has been collected by the German tax authority. As a result, investor A’s shares are now worth 19m (20m – 1m dividend).

- Investor A now sells these reduced-value shares, characterized as ex-divided shares, to investor C.

- As agreed before, investor C now delivers these shares to investor B. However, because they are worth 1m less, investor C pays investor B a dividend compensation worth €750.000,- and investor B’s bank provides him with a certificate to reimburse €250.000,- of dividend tax.

- Finally, investor B sells his shares (worth 19m) back to investor A. As a result, both investor A and investor B now own a certificate to reimburse the dividend tax, even though the German tax authority collected the tax only once.

- The additional reimbursed dividend tax is shared between investors A, B and C.

A Schematic:

Below is a simplified diagram of the basic alleged scheme:

{kind=link}

The alleged cum-ex scheme continues to make news. Reports indicate that hundreds of bankers, investors, consultants, and other individuals are under investigation and prosecutors have issued hundreds of subpoenas. The macro impact of the allegedly systematic, industrial-scale trading scheme remains to be seen. For more on the alleged scheme, see our prior post, The Biggest Tax Heist Ever? The Cum-Ex Scandal. For more on tax authority initiatives targeting international tax fraud, see J5 Continues its Effort to Identify International Tax Cheats.

White Collar Defense Attorneys

Freeman Law represents companies, executives, and individuals in regulatory and white-collar government investigations and prosecutions. We employ a proactive approach to defend vigorously and strategically position our clients. White-collar matters often involve parallel regulatory and civil proceedings. Freeman Law can navigate the complexities and collateral consequences of multiple proceedings. And when it comes to the court of public opinion, we employ ethical and strategic tactics to manage publicity. Schedule a consultation or call (214) 984-3000 to discuss your allegations and investigations concerns.